Ambraee Houslin | In defence of the NHT drawdown: the unglamorous arithmetic of building back

There is a particular kind of argument that wins applause in Jamaica precisely because it asks nothing of the person making it. The case against the National Housing Trust drawdown is one of them. It sounds principled. It invokes the worker, the first-time homeowner, the sanctity of a contribution deducted fortnightly from a payslip. And it conveniently sidesteps the only question that actually settles anything in public finance, which is not whether money should be spent on something good, but what you would have to do instead if you did not spend it this way. Every dollar the Government does not take from the Trust during this emergency is a dollar it must raise somewhere else, from someone else, on terms that are almost certainly worse.

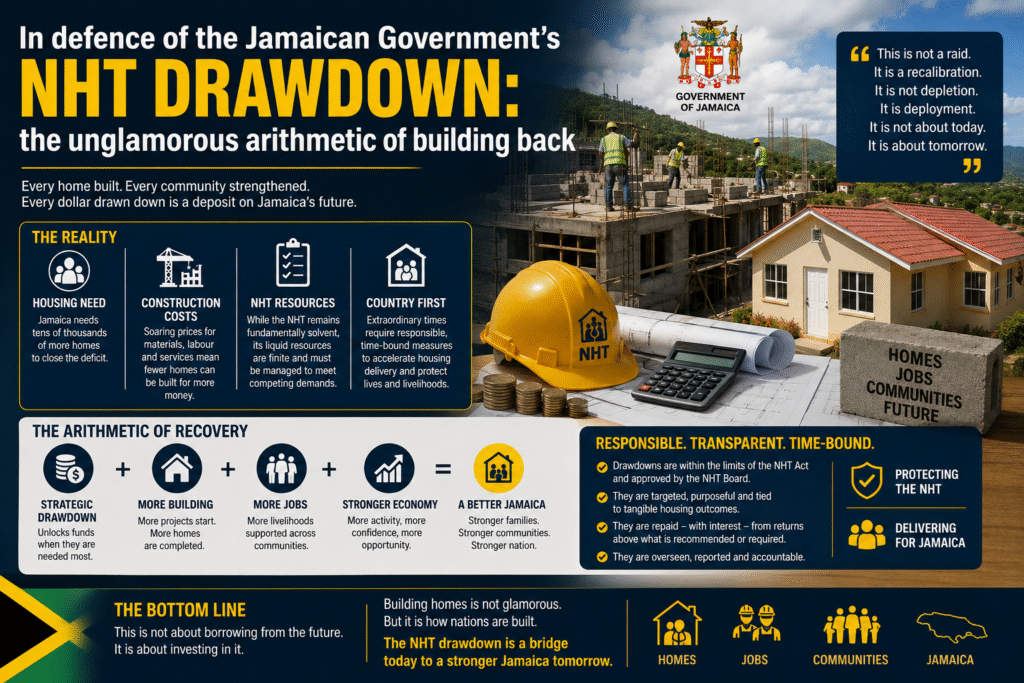

The Government will continue transferring 11.4 billion dollars a year from the NHT to the central budget, a measure now extended through the 2030/31 fiscal year. Over the past decade roughly 114 billion dollars has moved along the same channel. The Opposition has called the latest extension vulgar. The word does a great deal of work. It is meant to end the conversation before the arithmetic begins. So let us begin with the arithmetic, because the numbers are not on the side of the outrage.

At the close of the 2025/26 financial year, the NHT carried an accumulated surplus of about 185 billion dollars, a figure projected to climb toward 190 billion in the year ahead. Sit with that for a moment. The institution will continue lending 11.4 billion a year to the central budget and its surplus will still grow. Contributions have more than tripled since 2013, rising from 21.4 billion dollars to roughly 71 billion. Across that same stretch, the Trust has averaged annual surpluses in the order of 18 billion dollars, and it projects a further surplus of around 14 billion for the current year even after the withdrawal. An institution whose balance keeps rising while it lends to the recovery is not being hollowed out. It is being asked, during a moment of genuine national emergency, to put a portion of an idle balance to work.

The honest objection is not that the Trust cannot afford this. It is that the money belongs to contributors and ought to build houses. That concern is legitimate and deserves a direct answer rather than a rhetorical one. So here is the direct answer: homeownership has not been hampered by the transfer, and the record over the very years of the drawdown proves it.

Consider what the NHT has done for contributors while the withdrawals were ongoing. In 2025 the individual loan limit for open-market purchases was raised from 7.5 million dollars to 9 million. Two co-applicants can now access up to 17 million and three up to 23 million. A special limit of 12 million was introduced for single applicants buying homes priced at 14 million or less, the segment where ordinary Jamaicans actually buy. The construction loan limit for individual contributors rose to 11 million. The home improvement loan ceiling went from 3.5 million to 5 million, and the qualifying period shrank from ten years to seven. The Smart Energy loan moved from 1.5 million to 2.5 million, with interest rates restructured to run from zero to five per cent by income band rather than a flat five.

The list does not stop at loan sizes. Contributors earning less than 30,000 dollars a week saw their deposit requirement on qualifying open-market purchases cut to two per cent. Private-sector mortgagors, long treated less favourably than their public-sector counterparts, gained the right to apply their contribution refunds against existing mortgages and to draw refunds while servicing a loan. The Trust received a policy directive to concentrate its entire development pipeline on homes priced around 14 million or below. These are not the actions of an institution being starved. They are the actions of an institution expanding access to homeownership in the same years the Opposition insists it is being bled dry. Both things cannot be true, and the benefits schedule is not a matter of opinion.

This points to a fact that the housing debate consistently buries. The binding constraint on housing delivery in Jamaica has never been a shortage of cash in the Trust. It is construction capacity, contractor availability, the slow grind of land titling, and the planning approvals that turn a funded project into an occupied home. Redirecting every dollar of the drawdown back into housing tomorrow would not produce a single additional house this year. It would produce a larger idle balance sitting behind the same bottlenecks. The Trust already holds more capital than it can convert into completed units at the current pace of approvals and construction. Lending a fraction of that surplus to the national recovery costs contributes no house that would otherwise have been built.

Now place all of this against the event that reframes the entire debate. Hurricane Melissa struck in October 2025 as the most powerful storm to make landfall on the island in well over a century. Total damage and losses have been estimated at 12.2 billion US dollars, equivalent to roughly 57 per cent of the country’s 2024 gross domestic product. The economy contracted sharply in the final quarter of the year, with preliminary estimates pointing to a fall of between eight and thirteen per cent. Roads were severed, bridges weakened, and homes across whole parishes lost their roofs. Reconstruction is now expected to absorb high levels of resources for the first three to four years. This is the context in which the drawdown is being defended, and context here is not a footnote. It is the whole case.

And it sharpens the central question into one the Opposition prefers not to state plainly. If not the drawdown, then what? The alternative to drawing on national resources already in hand is not a costless act of restraint. It is one of two things, and both are worse. The first is higher taxes on the same workers, homeowners, small businesses, and consumers whose interests the measure is supposedly meant to protect. A drawdown from an institution sitting on a 185-billion-dollar surplus is plainly a less punishing instrument than a fresh levy on every household already absorbing higher post-storm prices. The second alternative is more borrowing, and that is where the deeper damage hides.

Jamaica did not arrive at this moment by accident. The country spent more than a decade hauling its debt down from levels that once exceeded 140 per cent of GDP to roughly 68 per cent, a discipline that turned it into one of the more credible sovereign stories in the region. That credibility is not sentiment. It is the reason that when Melissa struck, the Government could invoke the escape clause in its own fiscal rules, suspend the march to a 60-per-cent debt target, and have the Independent Fiscal Commission validate that the shock, assessed at 5.3 per cent of GDP across the recovery period, clearly cleared the threshold. It is the reason no major credit rating agency downgraded Jamaica after either the storm or the suspension. And it is the reason the country could assemble up to 6.7 billion US dollars in recovery financing from international institutions within weeks, on concessional rather than punitive terms.

Borrowing more aggressively at home would put precisely that achievement at risk. Every additional dollar the central government raises in the local market competes with the private sector for credit, pressures interest rates, and chips at the debt trajectory that the country bled for a decade to earn. Deploying a domestic resource already in hand, from an institution that is not spending it fast enough to exhaust it, is the move that protects the borrowing capacity rather than eroding it. The drawdown is not a departure from Jamaica’s fiscal discipline. It is an expression of it. It is the responsible lever pulled precisely so that the reckless ones do not have to be.

It is worth pausing on how the disaster financing actually worked, because it answers the charge that the Government simply reached for the easiest pot of money. The layered insurance framework built up over years did its job: the CCRIF payout delivered 14.3 billion dollars and catastrophe bonds returned a further 25.2 billion, while the IMF approved a 415-million-US-dollar emergency disbursement in January. The State drew first on the instruments designed for exactly this. The NHT drawdown sits inside that sequence, not in place of it, as one component of a deliberately diversified response rather than a lazy raid on the nearest balance.

None of this means the concern about permanence should be waved away. Contributors are right to expect that a transfer first framed as exceptional does not quietly harden into a permanent line in the budget. Even senators who backed the measure cautioned against making it permanent, and that caution is the line worth holding. The case for the drawdown rests entirely on Melissa being an extraordinary event, and an extraordinary justification cannot be stretched indefinitely without becoming a different argument altogether. The right posture is to support the measure now and to insist, loudly, that it expires when the emergency does.

The reconstruction ahead is also, if managed well, an opportunity rather than merely a bill. The experience after Hurricane Gilbert suggests that concentrated rebuilding in the first few years can lift productivity and pull activity forward, provided the money moves quickly and is matched by the institutional capacity to absorb it. Roads rebuilt to a higher standard, coastal towns reimagined rather than merely restored, housing stock replaced with more resilient construction: these are investments that compound for a generation. The capital has to come from somewhere. A portion of it resting in a national institution that cannot currently deploy it is a reasonable and far less painful place to look than the pockets of storm-battered households or the patience of the bond market.

So the defence of the drawdown is not a defence of raiding the workers’ trust, and it should not be argued as though it were. It is a narrower and far stronger claim. The Trust can afford it and its surplus still grows. Contributors are not losing houses, because loan limits, deposit terms, and benefits have all expanded through the very years of the withdrawal, and because cash was never the thing standing between Jamaicans and a home. And the alternative was never doing nothing. It was higher taxes or heavier borrowing, each of which lands harder on the same people the policy is meant to serve. Hold the line on permanence. Insist that the money moves and the houses rise. But spare the country the pretence that a free alternative was ever on the table. There was only the work of building back, and the unglamorous arithmetic of paying for it.

Ambraee Houslin is a Jamaican finance professional, private equity strategist, and columnist focused on capital markets, private investment, business growth, and economic development. He has worked across investment banking, corporate finance, mergers and acquisitions, and strategic advisory, supporting transactions across financial services, real estate, manufacturing, media, healthcare, and infrastructure.

Ambraee advises entrepreneurs, private companies, and investment groups on capital raising, acquisitions, business strategy, corporate structuring, and long-term value creation. His work focuses on helping businesses become more investable, scalable, and institutionally credible.

Syndicated from Our Today · originally published .

Legal context · powered by Jurifi

Get the legal angle on this story. Pick a prompt and Jurifi's AI will explain it using Jamaican law.

AI replies are based on Jamaican law via Jurifi. Not legal advice.

Other coverage

Peter Espeut | Raiding the house money

Jamaica Gleaner

‘Don’t make it permanent’ cautions Tavares-Finson while backing Govt’s decision to withdraw funds from NHT

Jamaica Observer

Editorial | NWC audit reveals a lie

Jamaica Gleaner

Danielle Archer | Jamaica’s democratic test has already begun

Jamaica Gleaner

Orville Taylor | To be global, host must be neutral

Jamaica Gleaner