Ambraee Houslin | The Caribbean’s debt-climate trap, and why Jamaica’s discipline may now work against it

There is a particular kind of unfairness that only shows up once a country has done everything it was told to do. Jamaica spent the better part of a decade and a half proving it could take fiscal medicine that most of the world assumed was politically impossible. Debt to GDP came down from levels north of 140 per cent to something closer to manageable. Primary surpluses were held even through periods of real hardship. The IMF programmes that once defined the country’s economic conversation became, improbably, a source of credibility rather than shame. And now, as the region’s multilateral institutions design the next generation of financing instruments meant to rescue Caribbean states from an intensifying cycle of debt and climate shocks, there is a real question as to whether Jamaica’s own success story leaves it standing outside the room where the new money is being allocated.

The scale of the underlying problem is not in dispute. The Caribbean Development Bank has put the region’s financing need at roughly US65 billion dollars over the coming decade, a figure that reflects not just conventional development spending but the compounding cost of rebuilding after storms that arrive with greater frequency and force than the fiscal architecture was ever designed to absorb. Annual resilience financing needs alone are estimated near US14 billion dollars, and by the Bank’s own reckoning, less than a tenth of that is currently being secured through existing channels. Five category five hurricanes in eight years is not an anomaly to be planned around. It is the baseline.

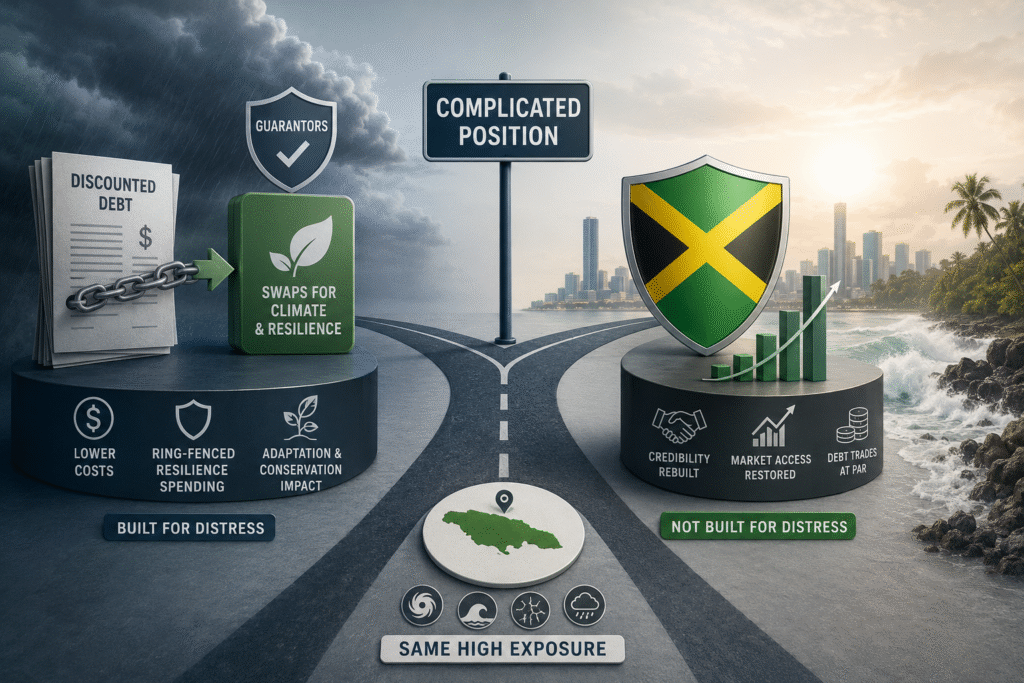

What makes this a structural problem rather than a temporary rough patch is the mismatch between how climate risk actually behaves and how the global debt architecture is built to respond to it. A hurricane does not show up as a liquidity event on a ratings model. It shows up as a multi-year drag on growth, a permanent revision downward in fiscal capacity, and a debt ratio that never quite returns to where it was. Jwala Rambarran, the former Central Bank of Trinidad and Tobago governor now advising the Caribbean Policy Development Centre, has argued that the architecture treats debt distress as episodic rather than structural, and that the G20’s Common Framework has consistently failed to deliver relief before countries have already absorbed the deepest domestic pain. His point about Jamaica is a pointed one. Both the 2010 and 2013 restructurings required years of adjustment before any meaningful relief materialised, a sequencing that punishes the country for the very discipline the international community says it wants to see.

This is where the new instruments become interesting, and where Jamaica’s position gets genuinely complicated. Debt-for-climate and debt-for-resilience swaps, the kind now being piloted with multiple guarantors backing reduced borrowing costs in exchange for ring-fenced resilience spending, are explicitly designed around distress. The Seychelles model that inspired much of this thinking involved buying discounted debt out of the hands of bilateral creditors and refinancing it on softer terms, with savings redirected into conservation and adaptation. That kind of arrangement makes sense when a country’s debt is trading below par because markets doubt it can pay. It makes considerably less obvious sense for a country whose paper trades reasonably well precisely because it rebuilt credibility the hard way. Jamaica is not the distressed case these instruments were built for, yet it carries almost identical physical exposure to the hazards these instruments exist to address.

The temptation is to read this as an argument against fiscal discipline, as though Jamaica would have been better served staying in distress long enough to qualify for concessional treatment. That would be exactly the wrong lesson. The more useful reading is that the region needs financing instruments calibrated to vulnerability rather than to default risk, which is the same point ECLAC and the Caribbean Development Bank have both been circling in their own language around a regional resilience fund. A framework that only rewards countries after they have exhausted their own adjustment capacity is a framework that punishes early responsibility. Jamaica, along with Barbados, has arguably the strongest claim in the region to demonstrate why vulnerability-based eligibility criteria matter more than debt-distress triggers, precisely because it has already proven what disciplined adjustment costs a small, hurricane-exposed economy and has little left to show for it in terms of access to the concessional pools now being built.

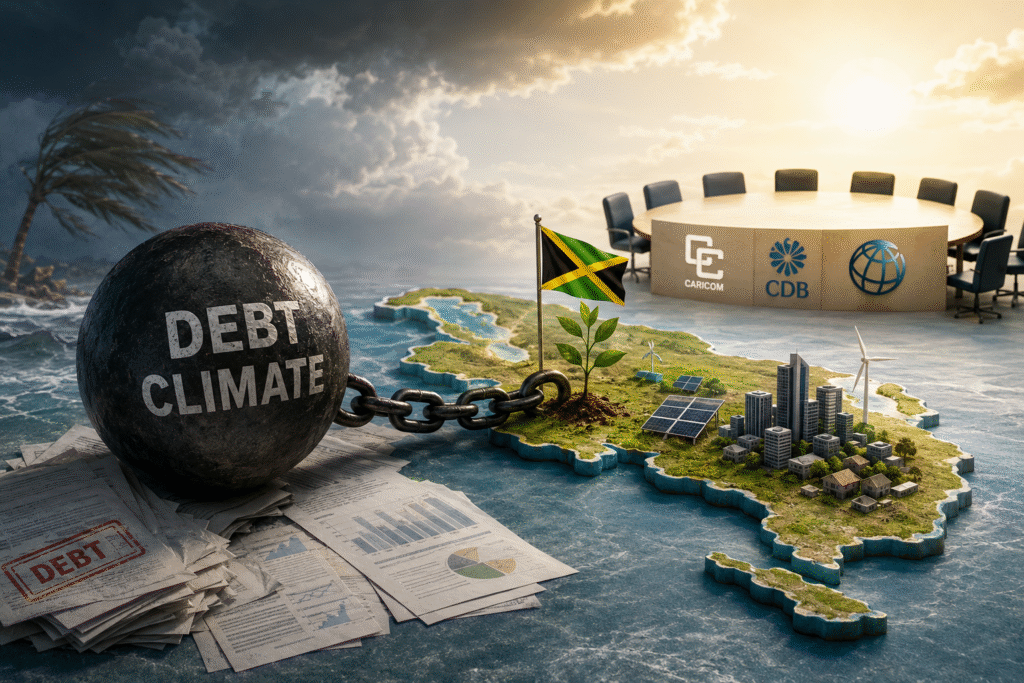

There is also a domestic capital markets dimension to this that deserves more attention locally than it currently gets. If regional resilience financing increasingly flows through guarantor structures, multilateral vehicles and pooled catastrophe instruments, Jamaican institutions, from the pension funds to the merchant banks to firms doing structured finance work across the region, have every reason to understand how these instruments are priced and where the arbitrage sits between concessional multilateral capital and what local markets currently charge for comparable resilience-linked paper. The Barbados Implementation Modalities pilot facility that opened earlier this year, with Jamaica among the eligible countries, is a small but concrete signal that this financing category is moving from conference-room theory into something with actual submission deadlines and actual dollars attached. Firms that understand the mechanics early will be positioned to advise on them. Firms that treat this as a policy story for economists will find themselves reading about the deals after they have already been done by others.

None of this resolves neatly. The Caribbean’s debt-climate trap is not going to be broken by a single instrument or a single pilot programme, and there is a legitimate case that Jamaica’s own path out of debt distress, however painfully achieved, remains the more durable model than betting the country’s fiscal position on financing structures still being tested elsewhere in the region. But the conversation happening right now among CARICOM finance ministries, the CDB and the multilateral development banks is one where the terms of eligibility are still being written. Jamaica has more standing than most to insist that discipline should be rewarded rather than quietly penalised in how that eligibility gets defined. Whether the country’s representatives show up to that conversation with that argument fully formed is, at this point, a genuinely open question.

Ambraee Houslin is a Private Equity Strategist with a strong background in economics and statistics. He has extensive experience in investment banking, corporate finance, and investment research across Jamaica and the Caribbean region. His core expertise includes mergers and acquisitions, capital structuring, and executing complex transactions that drive growth and value creation. Ambraee has led and supported deals spanning strategic acquisitions, private credit facilities, and post-transaction integration strategies for high-impact sectors.

Syndicated from Our Today · originally published .

Legal context · powered by Jurifi

Get the legal angle on this story. Pick a prompt and Jurifi's AI will explain it using Jamaican law.

AI replies are based on Jamaican law via Jurifi. Not legal advice.

Other coverage

Norris R. McDonald | ‘Dead money’ or prosperity? - Put Jamaica’s wealth to work

Jamaica Gleaner

Future-proofing Jamaica is more than just a slogan

Jamaica Observer

Suriname Energy, Oil and Gas Summit & Exhibition (SEOGS 2026)

Office of the Prime Minister

Diplomatic dilemma: Jamaica’s strategic choice

Jamaica Gleaner

The race for oil: will Jamaica be the next country to drill and what does that mean for its green pledges?

The Guardian (Jamaica)